Consumer-Facing Educational Materials

As an annuity professional, you understand the many roles fixed annuities can play in helping clients achieve various financial goals. At the same time, a great deal of misinformation about these products — and the professionals who sell them — exists, from false or misleading claims in the news to outdated perceptions passed down from previous generations of retirees.

NAFA has generated content and materials to help you educate consumers about fixed annuities by arming them with the truth. From fliers and brochures to whitepapers and media rebuttals, utilize the information below to assist your clients make better decisions about their retirement.

Continue checking back in the weeks and months to come as we add additional resources to this page!

Who Has Your Back? NEW!

In today’s shifting financial landscape, accumulation is only part of the retirement planning equation. This paper goes beyond the basics to highlight the protection systems that support fixed and fixed indexed annuities. Learn how insurer reserves, regulatory oversight and state guaranty associations work together to help provide long-term stability and peace of mind, even in uncertain times.

Risk Control Indices: Past, Present and Future NEW!

Since the 2008 financial crisis, the rise of passive investing has driven rapid innovation in index design, especially in the fixed indexed annuity (FIA) space. This paper explores the fundamentals of risk control indices, which use dynamic allocation between cash and risk assets to help deliver more stable returns over time. Learn how these indices work, how they can benefit annuity owners and what continued innovation means for the future of retirement planning.

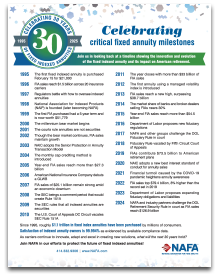

Celebrating the 30th Anniversary of FIAs

Though we’ve experienced significant changes related to FIAs throughout the last 30 years — from index crediting methods and riders to regulation and legislation — one thing hasn’t changed: the value of these products in helping consumers secure predictable lifetime income. Enjoy a timeline showing the innovation and evolution of the fixed indexed annuity and its impact on retirement.

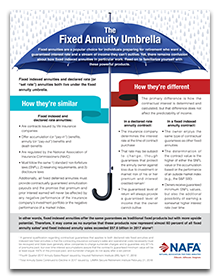

The Fixed Annuity Umbrella

Fixed annuities are a popular choice for individuals preparing for retirement who want a guaranteed interest rate and a stream of income they can’t outlive. Yet, there remains confusion about how fixed indexed annuities in particular work. This powerful piece concisely summarizes the similarities and differences between fixed, or declared rate, annuities and fixed indexed annuities.

Navigating the Choice of Fixed Indexed Annuities

Deferred annuities have become the Swiss army knife of retirement planning in academic as well as practitioners’ circles, with fixed indexed annuities (FIAs) dramatically growing in popularity in recent years. This paper examines carrier, index lineup and performance considerations that should form the backbone of a client’s (and agent’s!) decision in selecting an FIA. When combined with an analysis of other benefits, one can perform a comprehensive, independent evaluation and make choices with confidence.

ABCs of Indices

Indices have a key place in the financial ecosystem when it comes to measuring performance of particular aspects of the economy. In the context of retirement planning, both for saving and income purposes, indices have become a cornerstone of innovative annuity designs and applications. This paper seeks to provide ground-up education about important index terminology, various types of indices available on annuities and the role they play in generating interest as part of an accumulation strategy.

How to Make an Index

With so many indices available in today’s annuity marketplace, it can be difficult for consumers — and even some advisors — to determine which may be right for a particular retirement saver’s accumulation strategy. In the second paper of our Index Series, we look at the process of creating an index, including what are its “ingredients,” who is its target audience, and what tests and processes are necessary to perfect the index “recipe” to deliver maximum consumer benefit.

7 Reasons to Consider Annuities Now!

Given recent uncertainty, consumers are more interested in taking control of their finances and their future than ever before. Yet there is still considerable confusion about the value of fixed annuities and the role they can play as part of a holistic retirement plan. Discover seven of the most timely reasons to consider annuities when preparing for your future.

Download a copy of the resource »

¡Ahora disponible en Español! »

现已提供普通话版本 »

Annuities in Retirement Planning

Retirees are living longer, which means squeezing more out of their savings. Using annuities for retirement planning is different from a traditional financial planning approach but can provide unique features and benefits, including mitigation of certain risk factors. Learn how fixed annuities can boost the chances of retirement success through safe accumulation of interest and reliable income.

Annuity Crediting Strategies: Cap Strategy

Fixed indexed annuities (FIA) help consumers enjoy downside protection and upside potential in their retirement plans. Unfortunately, many are confused about the benefits of these products. NAFA seeks to break down specific features of these annuities in a way that anyone can understand. Learn how the point-to-point cap strategy works and why it’s a popular option available on many FIAs.

Annuity Crediting Strategies: Participation “Par” Rate Strategy

Many consumers are more familiar with how par can help their golf game than how par rate strategy can benefit their retirement nest egg. Fixed indexed annuities (FIA), and indexing in particular, are widely misunderstood and even misrepresented by some entities. This paper explains how the point-to-point participation rate strategy works and why it’s a popular option available on many FIAs.

Helping Consumers Understand FIAs

Fixed indexed annuities (FIAs), just like traditional fixed annuities, are insurance products that provide downside protection from loss of principal, with the potential for earning interest credits based on the performance of an underlying market index. In this report, learn how FIAs work and how they compare to other financial strategies for retirement planning, such as bond laddering or CDs.

Download a copy of the resource »

Product Comparison: Index-Linked Annuities

There’s more than one type of index-linked annuity. Two basic types that use an index and crediting strategy to determine account value are the fixed indexed annuity (FIA) and the registered index-linked annuity (RILA). This product comparison explains the key differences between these annuities and factors to consider when deciding which one would best fit in a consumer’s retirement plan.

The Anatomy of a Fixed Indexed Annuity

While some have made fixed indexed annuities (FIAs) out to be complicated, the reality is that they are sophisticated. This piece is designed to help consumers better understand the inner workings of FIA products, including how index crediting works, where your money goes, how rates are set, how insurers use the option budget and how renewal rates are determined. Greater education and understanding can help result in clearer expectations, allowing Main Street savers to determine how an FIA might fit into their retirement plans.

The Fixed Annuity Advantage

As baby boomers shift their focus from simply accumulating funds to turning accumulated funds into a reliable income, fixed annuities have evolved to address both these challenges. This piece offers agents and consumers information on the guaranteed lifetime income, or withdrawal, benefit available on these powerful products.

9 Answers Every Investor Needs to Know about Annuities

Many consumers have received or been asked to download information about annuities produced by someone who doesn’t sell them or who doesn’t believe you should buy or own them. Much of this information is misleading; some of it warrants four Pinocchios! The information in this document is intended to provide readers the facts contrary to the negative sales pitch. Facts are empowering! With them, consumers can make informed decisions about their financial goals and retirement plan.

The Power of Words

Fixed annuities offer a unique and attractive blend of safety, growth potential, tax advantages and lifetime income — which may make them a good fit for many clients. Yet appreciating the true power and capabilities of fixed annuities requires understanding the key terms that are used to define them. Use this flier as a handy guide for educating your clients about the basics of fixed annuities and annuity terminology.

Download a copy of the resource »

Download a copy of the Alliance for Lifetime Income Annuities Language Glossary »